Introduction — Why this matters to you

Imagine counting on a steady Social Security check in retirement and then finding out it may be smaller than expected. That worry is real for many Americans because of ongoing concerns about social security trust fund depletion. Whether you are a retiree, a worker decades from retirement, or a policymaker, understanding what the trust fund does, why it could run short, and what options exist is essential to planning and decision-making.

What is the Social Security trust fund?

The phrase social security trust fund actually refers to two reserves managed by the Social Security Administration: the Old-Age and Survivors Insurance (OASI) trust fund and the Disability Insurance (DI) trust fund. Collectively they are often called the OASDI or simply the Social Security trust funds. These funds hold surplus payroll tax receipts and invest them in special-issue Treasury securities that the federal government redeems to pay benefits when payroll-tax income isn’t enough.

How did we get here? Causes of trust fund depletion

Several structural and demographic trends have combined to produce the trust fund shortfall pressure.

Demographic shifts

- Baby boomer retirements: A large generation is moving into retirement, increasing the number of beneficiaries.

- Longer life expectancy: People are living longer, so benefits are paid over more years.

- Lower birth rates: Fewer workers entering the workforce reduces the number of payroll taxpayers per beneficiary.

Revenue and benefit structure

- Payroll tax rate limits: The current payroll tax rate and taxable maximum are set by law and haven’t kept pace with rising costs.

- Wage growth vs. benefit growth: When benefits and indexed adjustments outpace the revenue base, shortfalls widen.

Economic and policy factors

- Economic cycles: Recessions reduce payroll tax collections and can temporarily increase claims.

- Disability claim trends: Higher or lower DI claims affect reserves separate from OASI.

- Policy choices: Past decisions to borrow from trust fund balances for other federal spending have left the funds holding Treasury IOUs rather than diversified assets.

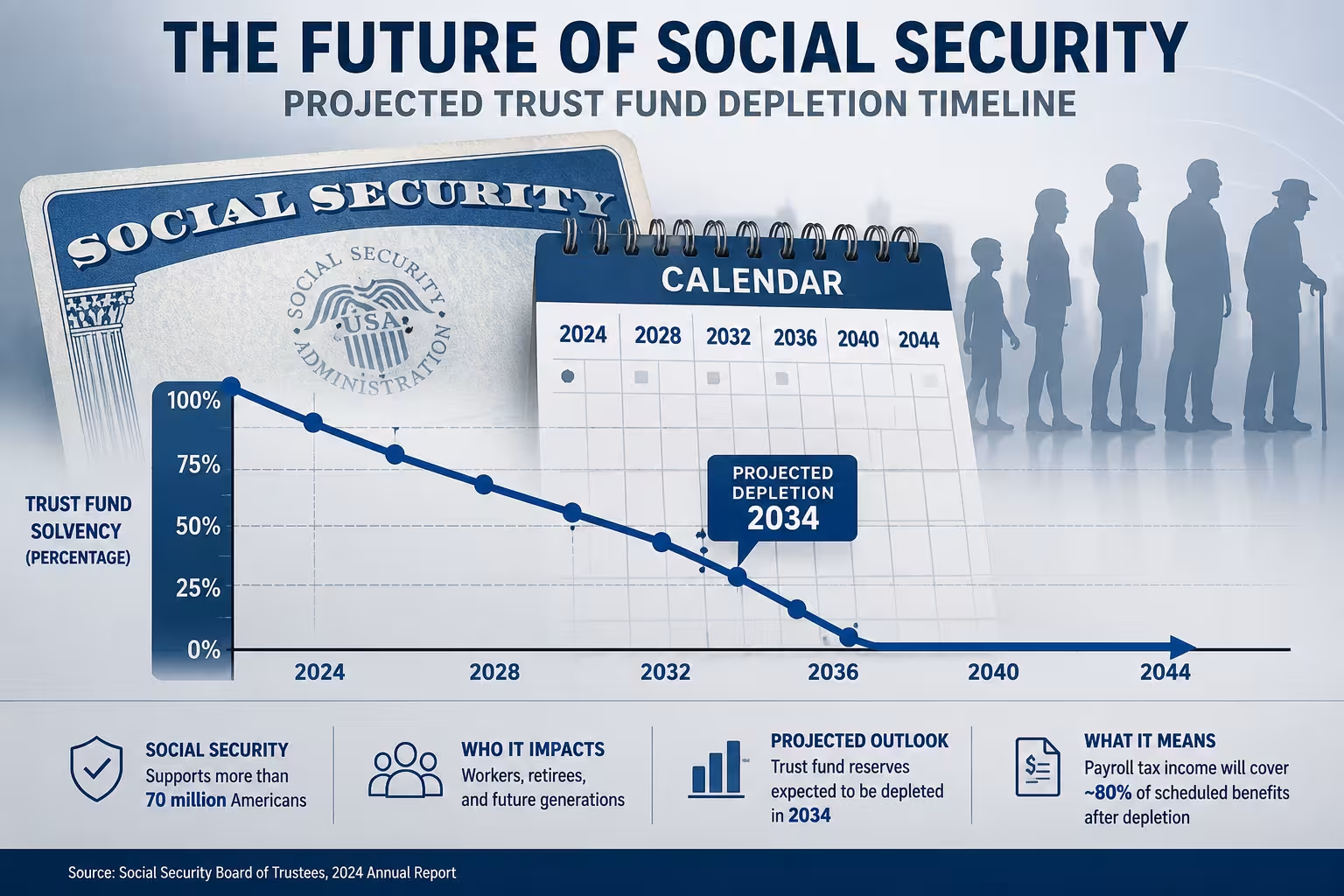

Timeline: When could depletion happen?

Projections vary year-by-year because they depend on economic and demographic assumptions. Recent trustees reports have warned that, under current law and typical projections, the combined Social Security trust funds face significant shortfalls within the next decade or two. Exact dates change as assumptions about employment, wages, fertility, and longevity are updated.

Key things to know about the timeline

- Depletion means trust fund reserves are exhausted; payroll taxes would still fund a portion of scheduled benefits.

- Even after reserves are depleted, benefits do not automatically disappear—Congress has options, and automatic benefit reductions from payroll tax revenue shortfalls would likely be partial, not total.

- Projections are not fixed dates but warnings based on current law; policy changes can move the date outward or inward.

What happens if the funds are depleted?

If trust fund reserves are depleted and Congress doesn’t act, Social Security would be limited to paying out what incoming payroll taxes can cover. Historically, projections show that payroll-tax income might cover somewhere between about 70% and 80% of scheduled benefits depending on the year and assumptions. That gap would mean automatic cuts unless policymakers implement reforms or new revenues are provided.

Short-term and long-term consequences

- Reduced benefits for current and future beneficiaries if no legislative fix is passed.

- Increased uncertainty for middle- and low-income retirees who rely heavily on Social Security.

- Potential political pressure to accelerate benefit cuts or raise taxes, which could be disruptive.

Policy solutions: How lawmakers can address the shortfall

There is no single fix; most proposals blend revenue increases, benefit changes, and structural reforms. Here are common options:

Revenue solutions

- Raise the payroll tax rate (employee and employer shares).

- Raise or eliminate the taxable maximum (the wage cap above which earnings are not taxed for Social Security).

- Redirect new or general revenues to Social Security on a temporary or permanent basis.

Benefit and eligibility changes

- Gradually raise the full retirement age to reflect longer lifespans.

- Change the cost-of-living adjustment (COLA) formula to slow benefit growth.

- Means-testing benefits or modifying the benefit formula to be more progressive.

Structural reforms

- Blend OASI and DI finances differently or maintain separate streams with policy tweaks.

- Adjust how benefits are calculated (e.g., indexing more to prices vs. wages).

- Expand investment options for trust fund assets—controversial because it introduces market risk.

Most experts recommend a mix of modest revenue increases and targeted benefit changes phased in over time to reduce hardship and spread the burden across generations.

What you can do: Practical steps for retirees and workers

While policymakers decide on broader reforms, individuals can take concrete steps to protect retirement security.

Actions for workers

- Start or increase retirement savings in 401(k)s, IRAs, or other tax-advantaged accounts.

- Delay claiming Social Security to increase monthly benefits if you can afford to wait.

- Diversify income sources: investments, part-time work, rental income, and annuities can supplement Social Security.

- Maximize employer retirement matches and minimize high-fee investments.

Actions for near-retirees and retirees

- Run multiple benefit-claiming scenarios to decide the best claiming age.

- Consider annuities or laddering bond/CD maturities to secure income if you fear cuts.

- Trim discretionary spending, review budgets, and prioritize essential costs like housing and healthcare.

- Consult a fiduciary financial planner to integrate Social Security projections into your broader retirement plan.

FAQ — Common questions about social security trust fund depletion

Will Social Security disappear when the trust fund is depleted?

No. Depletion means trust fund reserves are exhausted and the program would rely solely on incoming payroll taxes. That typically funds a substantial portion, though not all, of scheduled benefits. Congress can also intervene with reforms or new revenue.

How much could benefits be cut?

Projected replacement rates vary depending on payroll tax income. Historically, estimates suggest reductions could be in the range of roughly 20–25% of scheduled benefits if no changes are made, but the exact figure depends on future earnings and policy decisions.

Should I claim benefits earlier because of the risk?

Claiming earlier reduces your monthly benefit permanently. In most cases it’s better to plan based on your personal health, financial need, life expectancy, and other income sources rather than making a blanket decision to claim early because of uncertainty about the trust fund.

Is the trust fund invested in stocks?

No. Trust funds currently hold special-issue Treasury securities. Some reform proposals suggest diversified investments, but these introduce market risk and political debate.

How can I stay updated on the latest projections?

Watch the annual Social Security Trustees report and independent analyses from the Congressional Budget Office, Congressional Research Service, and reputable think tanks.

Authority and further reading

Understanding the details matters. Review these authoritative sources for the most current projections and policy analysis:

- Social Security Administration Trustees Report (annual)

- Congressional Budget Office reports on Social Security and budget outlook

- Congressional Research Service analyses and briefs

- Independent policy research from Brookings, Urban Institute, and Center on Budget and Policy Priorities

Conclusion — Planning beats panic

Social security trust fund depletion is a serious fiscal challenge, but it is not an immediate cliff that wipes out benefits overnight. The trust fund projections are a call to action for policymakers and a reminder for individuals to build resilient retirement plans. By understanding the causes, monitoring policy developments, and taking practical steps—saving more, diversifying retirement income, and making informed claiming decisions—you can reduce risk and increase financial confidence regardless of Washington’s timetable.

If you want, I can run personalized claiming scenarios, suggest a retirement savings checklist, or summarize the latest trustees report and what it means for your expected benefits. Which would you prefer?