Budgeting is usually a confusing puzzle of spreadsheets and deprivation. For most, it’s the fiscal version of a New Year’s Resolution—wonderful intention, poor execution.

But what if there were a single easy, adjustable rule that could steer your spending and saving without you having to account for every last penny?

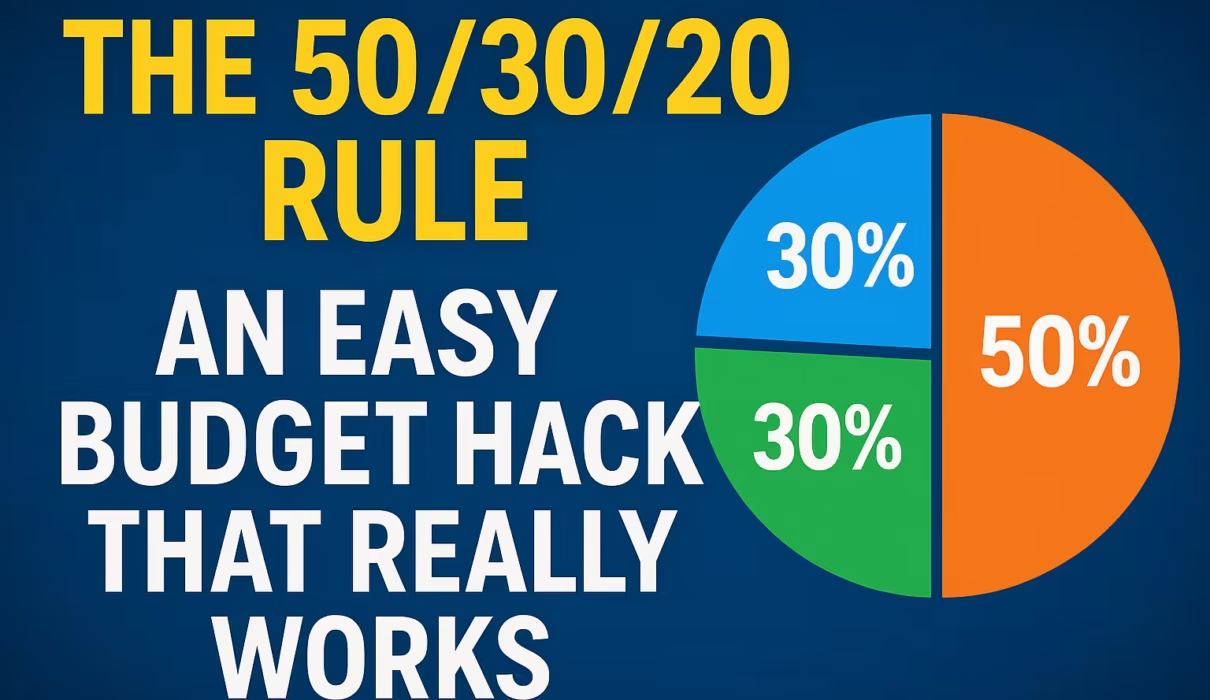

Enter the 50/30/20 Budgeting Rule.

This impressive, intuitive system is one of the most widely used budgeting tools for a reason: it’s straightforward, simple to use, and instantly scalable to any income.

What is the 50/30/20 Rule?

The 50/30/20 Rule is a basic rule of thumb for allocating your after-tax income (your take-home pay) into three broad spending categories:

| Percentage | Category | Description |

| 50% | Needs | Essential, non-negotiable expenses required for survival and stability. |

| 30% | Wants | Discretionary, non-essential expenses that improve your quality of life. |

| 20% | Savings & Debt | Financial future expenses, including saving for retirement or paying off high-interest debt. |

Here is what should go in each category:

1. Needs (50% of Income)

These are the things you have to pay to keep living your lifestyle. If you didn’t pay these, your lifestyle would be greatly disrupted.

Housing: Rent/mortgage payments, property taxes.

Utilities: Electricity, gas, water, basic phone/internet service.

Groceries: Groceries at home (not eating out).

Transportation: Car loans/gas/insurance, public transportation fees.

Minimum Debt Payments: The minimum payments on credit cards, student loans, etc.

Essential Insurance: Health insurance.

The Rule: Have all your vital “Needs” account for less than 50% of your take-home income. If your needs regularly clock more than 50%, the model indicates that you’ll need to cut your cost of living (for example, getting a lower rent or transport).

2. Wants (30% of Income)

These are your discretionary expenditures that you splurge money on. Though they may feel like they’re needs, they are things that you could actually survive without.

Entertainment: Streaming services (Netflix, Spotify), concerts, films.

Dining Out: Restaurants, coffee shops, and takeout.

Hobbies and Travel: Gym memberships, vacations, clothing outside the necessities.

Upgrades: High-end TV/internet plans, latest smartphone, a more luxurious car than you require.

The Rule: Spend 30% of your income on these categories. This is your fun money—spend it guilt-free! Having a generous amount set aside for “Wants” is what makes this rule workable and achievable.

3. Savings & Debt Repayment (20% of Income)

The single most important category for your long-term financial well-being. This 20% automatically goes to future-oriented goals.

Savings: Amounts saved in retirement savings accounts (401k, IRA), emergency fund, and down payments.

Extra Debt Payments: Any amount paid over the minimum debt payments for items such as credit cards, student loans, or auto loans.

The Rule: Save 20% for your future finances. This guarantees you’re always accumulating wealth and paying off debt, building a solid retirement and emergency fund foundation.

How to Apply the 50/30/20 Rule to Your Salary

The best aspect of the 50/30/20 rule is that it is percentage-based, so it will function whether you make $30,000 or $300,000. But life isn’t always equal, and the rule must be adaptable:

Scenario 1: High-Debt or Low-Income Earners (The “40/30/30” Pivot)

If you owe a lot of high-interest consumer debt (such as on credit cards) or your pay is low, that whole 20% for savings may seem out of reach.

Adaptation: Briefly boost the Savings/Debt category by borrowing from “Wants.” For instance, use a 50/20/30 split with 30% going toward paying off debt aggressively until all high-interest debt is paid off. After the debt is cleared, the 30% can go back to the standard 20% savings and 30% wants.

Scenario 2: High-Income Individuals (The “30/30/40” Pivot)

If your earning capacity is high, your basic “Needs” may absorb only 30% or 40% of your after-tax income.

Adjustment: Transfer the unused amount from “Needs” to Savings. A deep-pocketed saver may prefer a 30/30/40 ratio, saving 40% of income, enabling them to reach retirement objectives much earlier.

Getting Started in Three Simple Steps

Calculate Your Monthly Take-Home Pay: Locate your pay stub and determine your income after taxes and deductions. This is your total budget number.

Determine Your Target Allocations:

50% * Take-Home Pay = Needs Target

$30 * Take-Home Pay = Wants Target

20% * Take-Home Pay = Savings Target

Audit Your Current Spending: Take a look at your bank statements for the previous month. Do your actual spending figures fall into these target categories? If not, see which category is over-spent and develop a plan to shift (typically by reducing “Wants”).

The 50/30/20 Rule isn’t a strict law, but an empowering thought process. It makes budgeting easy, makes you balance your current enjoyment with your future safety, and provides you with a clear road map to financial independence.